What is Optional Coverage in Health Insurance, what are its benefits?

Introduction

Apart from the basic coverage in Health Insurance, there are also optional coverage in health insurance Let’s know what are its advantages and disadvantages, you will get complete information in this blog.

For this optional Coverage in Health Insurance, you have to pay extra for which you get its benefits.

Some examples are:-

- Super NCB

- Non-Medical Expenses Rider

- Cancer Rider

- Critical Illness Rider

- Personal Accident Rider

- Unlimited Reload

- Maternity Benefits

- OPD Expenses Rider

- Hospital Daily Cash benefits

- International Cover

- Premium Waiver

- Inflation Protector

- NCB Protector

- Reduce waiting for Pre- Existing Diseases Rider

- Vaccination Cover

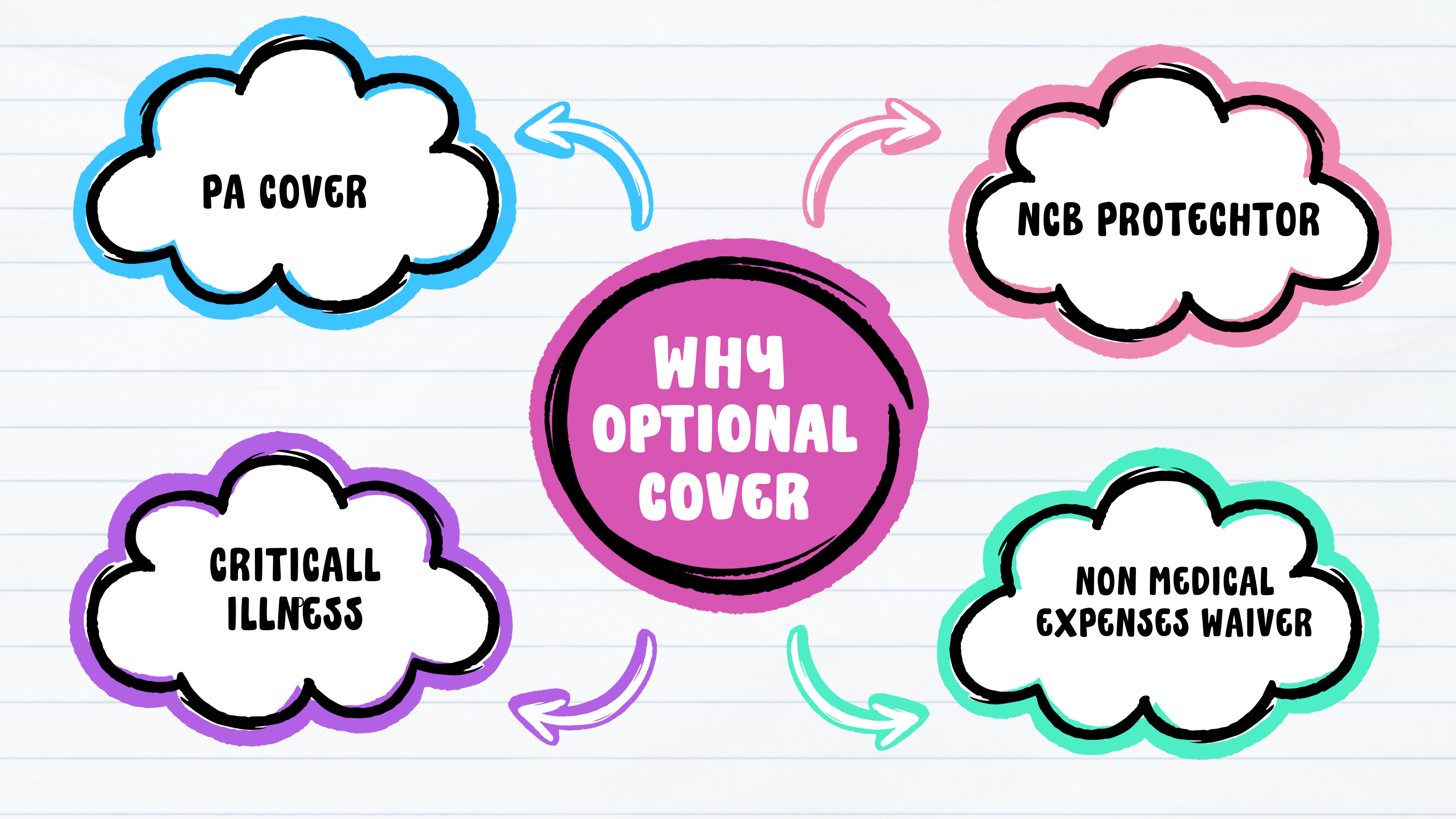

Super NCB:-

Before understanding this we have to understand NCB. When our policy is claim-free in a year i.e. there is no claim in our policy and whenever we renew the policy, some additional bonus is added to our existing cover, which we call NCB, which is according to every plan. It can be different like 10%, 20%, 50% etc.

This NCB is available on the basic sum insured by our health policy. Now if we want an additional bonus on top of this bonus, then we can take the option of Super NCB, but one thing should always be kept in mind that we get the benefit of Super NCB only for 2 years but the additional premium will be given to us lifelong, on every renewal.

Non- Medical Expenses Rider:-

The insurance company does not bear all the expenses of the claim such as needles, syringes, cotton, and urine containers etc., all the companies give a rider for this on an additional premium which is called safe-guide, health guide etc. By taking these options, the insurance company Also gives claims, but there are some expenses for which even these riders do not work, such as Hospital Registration Charges, Medical Records Custodian Charges etc. Advice: This rider should be in your policy.

Cancer Rider:-

Cancer booster rider in insurance plans is used for cancer hospitalization and the cover is not deducted from the base sum insured its cover is different in each insurance company, like in the case of cancer hospitalization, double the basic cover in any insurance company. Cover is provided and its premium is not high.

Critical Illness Rider:-

This is a kind of Fixed Benefits Rider in which the insured person gets the money off this rider due to a Listed Critical Illness, you can take it as an additional policy, my advice for this is that you can take it as an additional policy. Take it as it is.

Personal Accident Rider:-

This is also a Fixed Benefits Rider which is useful in case of any accident, but in this rider, only two benefits are available in case of death or complete disability due to an accident, my advice for this is that you should take it as a standalone product only.

Unlimited Reload:-

When Basic Sum Insured gives cover for unlimited times then it is called Unlimited Reload, this risk can be taken any number of times till the Cover Date, let us assume that Mr A has 10 lakh Basic Cover i.e. Mr A cover of up to Rs 10 lakh can be availed per hospitalization.

Maternity Benefits:-

This coverage in Health Insurance sounds quite good. Whereas, Maternity does not work in the principle of insurance, understand it like this out of 100 married couples, only 10 do not have a baby, then 90 will have to pay a Maternity Claim i.e. confirm a high claim ratio, in this situation the Company will pay the sum insured. Keeps the same premium. No one should take this rider.

OPD Expenses Rider:-

In this, for any treatment for which we are hospitalized for 24 hours or more, we can get reimbursement of OPD expense bills under Pre-Post Benefits. Without hospitalization for 24 hours, we will not get the claim of OPD Expenses. By taking this rider we can claim as per OPD limits.

Hospital Daily Cash benefits:-

The insurance company provides the facility of hospital cash benefits with an additional premium in which 24 hours of hospitalization is necessary and the insurance company does not give hospital cash benefits for the first 24 hours i.e. a maximum of 10 days one hospitalization or whatever is as per the plan. She is the one who gives. It can range from Rs 500 to Rs 5000 or even more.

International Cover:-

Many companies offer the option of International Cover as a standalone plan a rider or both, in which the treatment is done abroad.

Premium Waiver:-

Many companies provide this facility as an inbuilt feature in their plans and some as an optional rider in the form of an additional premium, in which in the case of some listed Critical Illnesses, the insured does not have to pay the next year’s premium and the policy is automatically renewed. My advice is that you should give priority to the inbuilt policy only. One more thing to keep in mind is that the benefit of this rider can be availed only once or twice in the entire policy period, for this please check the policy wording once.

Inflation Protector:-

These riders are based on very complex calculations, such as when inflation increases, your sum insured increases as per inflation.

NCB Protector:-

When you pay an additional premium for this rider, your No Claim Bonus does not reduce as per certain claim limits and you also get the bonus on the next renewal. Let us understand this with an example, say Mr A has a health insurance policy of Rs 10 lakh and he has taken NCB Protector rider and his claim comes only up to 25% of the Base Sum Insured (this may vary according to the plans). If so then they get NO Claim Bonus on renewal next year.

Reduce waiting Pre- Existing Diseases Rider:-

Like in health insurance, if there is any pre-existing disease, then there is a waiting period for it. It can be 24, 36, or 48 months, but if we can reduce this waiting period, we can do it with an additional premium.

Vaccination Cover:-

Although there are some vaccination covers in the Health Insurance Plan, by opting for this rider, you get the claim for whatever vaccination is approved for any pandemic as per the limits of the rider, you should not opt for this rider because you have to pay for every vaccination. We have to pay an extra premium on renewal and rarely do we claim it.

Conclusion:-

Whenever you take health insurance, definitely consult an expert, and you have to decide for yourself which optional cover to take, this article of mine will be useful as a reference, so definitely refer to it once. Your feedback will make our content better, so please give your feedback. Share this article as much as possible.

Contact Us for more Information: Click Here